GSTR 1 : Filing, Format and Due Dates

Published on: Thu Aug 29 2024

Sonu Gupta

What is GSTR 1 ?

The Goods and Services Tax Return 1, or GST Return 1, is a form that businesses must fill out each month or quarter. This form lists all the sales and services the business provided during that time. However, some people don’t need to fill it out, like businesses that pay a flat tax rate (called composition vendors), foreign businesses not based in the country, and those with a special identification number.

GSTR 1- Filing, Format and Due Dates

The Goods and Services Tax Return 1, or GST Return 1, is a form that businesses must fill out each month or quarter. This form lists all the sales and services the business provided during that time. However, some people don’t need to fill it out, like businesses that pay a flat tax rate (called composition vendors), foreign businesses not based in the country, and those with a special identification number.

GSTR 1 Due Date

Starting January 1, 2021, small businesses with total sales under 5 crores can opt to file their GST returns for every quarter instead of every month. They need to submit their GSTR 1 return by the 13th of the month after each quarter ends. However, they can still send in their invoices every month if they want to via the invoice furnishing facility (IFF) every month.

Essential for filing GSTR-1

- The business must be registered under GST with a 15-digit GSTIN based on their PAN.

- Detailed invoices with unique serial numbers are required for all transactions:

- Intra-state (within the same state)

- Inter-state (between different states)

- Business-to-business (B to B)

- Retail (B to C)

- Exempted and non-GST supplies

- Stock transfers between locations in different states

- To verify the GST return, one of the following is needed:

- OTP from the registered phone (for EVC)

- Digital signature certificate (class 2 or higher)

- Aadhar-based e-sign

How to file GSTR 1 ?

The GSTR 1 form includes different sections that collect information about a business’s sales and supplies. Here’s a simple breakdown:

- The first part asks for the year and the specific time period for which the form is being filled out.

The other parts ask for details about the taxes related to sales and supplies during that time.

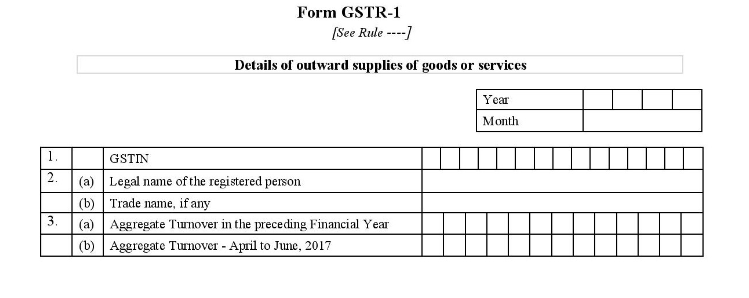

1. GSTIN: your unique PAN-based 15-digit Goods and Services Taxpayer Identification Number

2. Name of the taxpayer:

- Registered Person legal name

- Trade Name

3.Turnover of the Taxpayer:

- Aggregate turnover in the previous year: This is the total amount of sales and supplies your business made in the year 2016-2017, before taxes. You only need to provide this information for that year. In the future, this number will be calculated and filled in automatically.

- Aggregate turnover from April to June 2017: This is the total value of your sales and supplies from the beginning of the fiscal year until the GST system started.

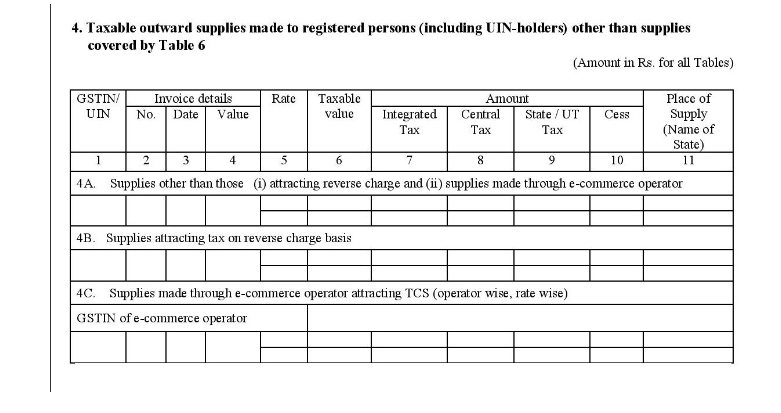

4.Taxable outward supplies made to registered persons (including UIN holders) excluding the contents of table 6:

- Details of taxable B2B supplies: List all business-to-business sales made during this tax period. Exclude any sales that involve reverse charge (where the buyer pays the tax) and sales made through online platforms like Amazon or Flipkart. For each sale, provide a breakdown of the Central GST (CGST), State GST (SGST), and Integrated GST (IGST).

- B2B sales with reverse charge: Include sales where the buyer is responsible for paying the tax, such as services from a goods transport agency or taxi services arranged through an online aggregator.

Online sales through e-commerce channels: Report sales made through e-commerce platforms like Amazon or Flipkart. Organize the data according to the GSTINs of the e-commerce operators or channels involved.

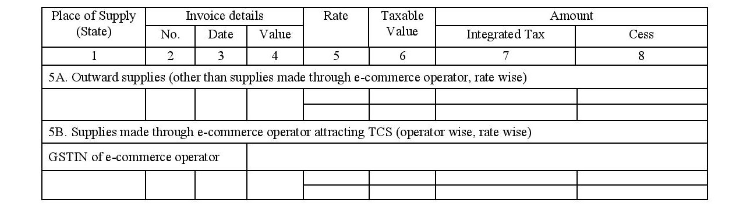

5.Taxable outward inter-state supplies to an unregistered consumer where the invoice value is more than Rs. 2.5 lakh:

- Sales to large consumers or unregistered businesses: This part is for listing sales where the invoice amount is more than 2.5 lakh rupees or sales to businesses that are not registered for GST.

- B2C and B2B sales details: Include details of sales made to end consumers and unregistered businesses in different states, but not through e-commerce platforms.

- Online interstate B2C sales: Provide details of sales made online to end consumers in different states. This should include where the sale took place, the taxable value, and the GSTINs of the e-commerce operators involved.

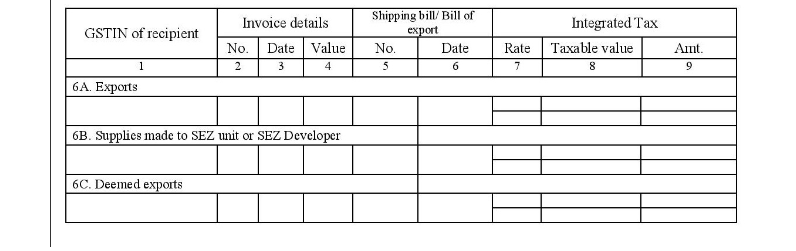

6. Zero-rated supplies and deemed exports:

- Exports: List all the exports made during the tax period. Include invoice details, shipping bills, and any taxes related to these exports.

- Supplies to SEZ: Report any supplies made to customers in Special Economic Zones (SEZ), whether to SEZ units or SEZ developers.

- Deemed exports: Provide details of transactions treated as exports even though the goods are still within the country. This includes supplies to export-oriented units, technology parks, or government-funded projects, and payments made in Indian Rupees (INR) or foreign currency equivalent to INR.

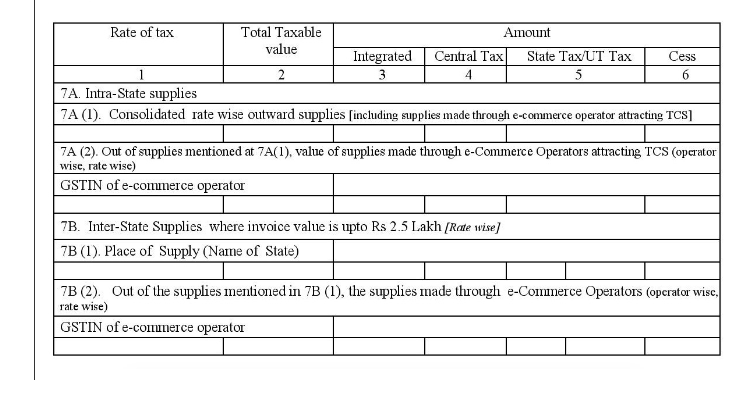

7.Taxable supplies (net of debit notes and credit notes) to unregistered persons, other than supplies covered under Table 5:

This table captures a rate-wise summary of sales and supplies made for the tax period including taxable value and the tax collected under various heads.

- Intrastate supplies

a.Consolidated details of B to C sales (both online and offline).

b.Online B to C sales. Provide the GSTIN of the e-commerce operator(s) involved.

- Interstate supplies where the invoice amount is less than Rs. 2.5 lakh

a. Details of B to C interstate supplies along with the place of supply.

b. Details of B to C interstate sales made online. Provide the e-commerce operator’s GSTIN.

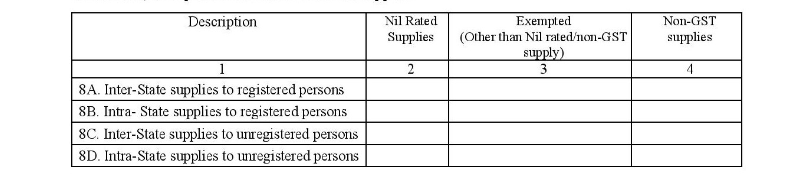

8. Nil rated, exempt, and non-GST outward supplies:

Capture the sales summary of items and/or services that are nil rated (0% GST but allow you to claim ITC on tax paid for inputs), exempt (those which do not attract GST but do not allow you to claim ITC on tax paid for inputs) and non-GST supplies (those which are outside the purview of GST and may attract other taxes like state VAT).

- Interstate supplies made to registered persons: B to B sales made to GST registered businesses in other states

- Intrastate supplies made to registered persons: B to B sales made locally (to GST registered businesses located in the same state).

- Interstate supplies made to consumers and unregistered persons: B to C sales made to customers and unregistered businesses located in other states.

Intrastate supplies made to consumers and unregistered persons: B to C sales made locally (Includes end consumers and unregistered businesses).

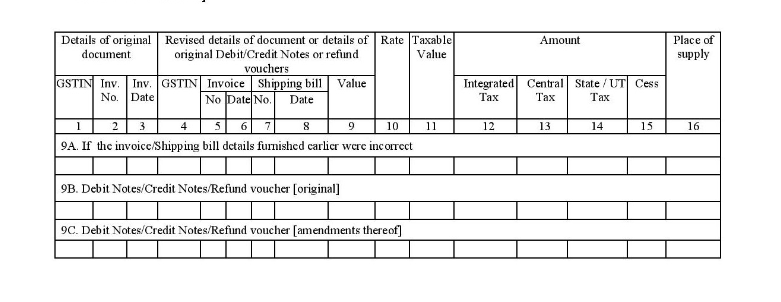

9. Amendments to taxable outward supply details furnished in returns for earlier tax periods in table 4, 5 and 6 (including current and amended debit notes, credit notes, and refund vouchers):

1.Updating Past Sales Records:

- Making changes or fixing errors in the sales records you submitted in earlier tax periods.

2. Incorrect Invoices and Shipping Bills:

- Details of invoices and shipping bills from previous returns that were incorrect, along with how you are correcting them.

3. Original Debit Notes, Credit Notes, and Refund Vouchers:

Information about new debit notes, credit notes, and refund vouchers created during the current tax period.

4. Changes to Debit Notes, Credit Notes, and Refund Vouchers from Earlier Periods:

Details of any updates made to debit notes, credit notes, and refund vouchers from previous tax periods. Include information like the original document’s GSTIN, number, date, and other relevant details.

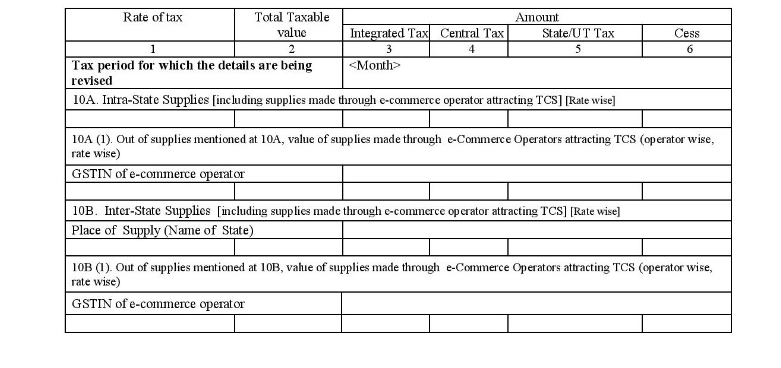

10. Amendments to taxable outward supplies to unregistered persons furnished on returns for earlier tax periods:

- Changes to Local Sales: Updates or corrections to sales made within your state during previous tax periods. This includes changes to both online and offline sales, along with the GSTINs (tax identification numbers) of everyone involved.

Changes to Out-of-State Sales: Updates or corrections to sales made to businesses or customers in other states during previous tax periods. This includes changes to both online and offline sales, and the GSTINs of the parties involved.

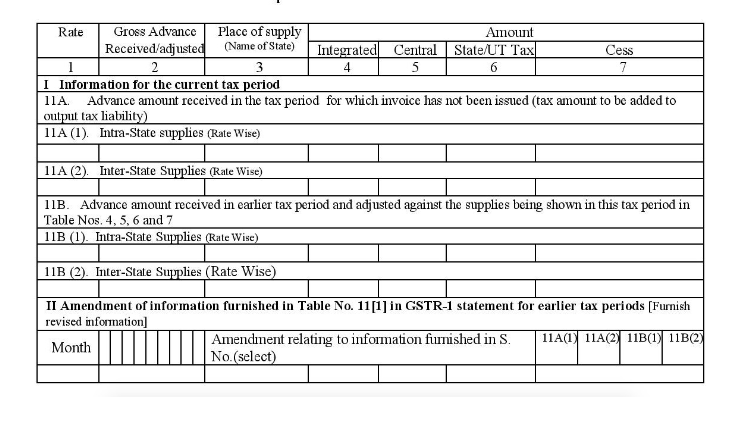

11. Consolidated Statement of Advances Received or adjusted in the current tax period, plus amendments from earlier tax periods

Advance Payments Received This Period:

- Any money you received in advance during this tax period for sales that you haven’t invoiced yet. This includes both sales within your state and sales to other states.

Advance Payments from Previous Periods:

- Money you received as advance payments in earlier tax periods that you are now using to cover sales made in the current tax period.This includes any adjustments listed in tables 4, 5, 6, and 7.

Updates to Previous Returns:

Any changes or updates made to the information from earlier tax returns as per subsection 11A.

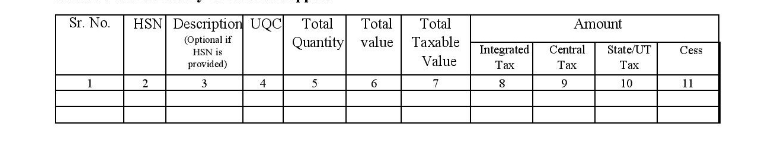

12. HSN-wise summary of outward supplies:

In this section, you need to provide a clear summary of the items you’ve sold, organized by their HSN (Harmonized System of Nomenclature) codes. For each HSN code, list the total quantity of items sold and the total taxable value of those items. Additionally, if the items are being exported or imported, include the Unit Quantity Codes for these transactions. This helps in tracking and reporting your sales accurately based on the classification of your products.

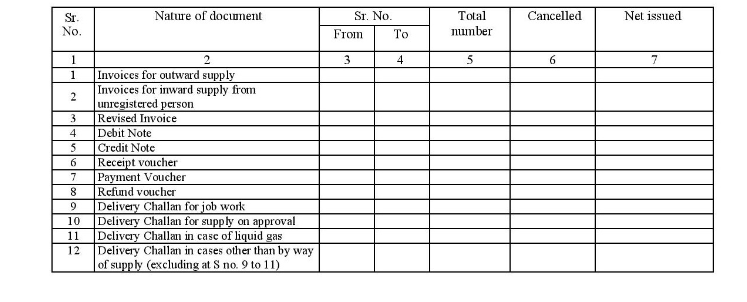

13. Documents issued during the tax period:

1.Sales Invoices:

The bills you give to your customers when you sell something. They include a unique serial number, customer details, the current status of the invoice, and how many invoices you issued for the tax period.

2.Invoices for Purchases from Unregistered Vendors:

Bills you get from vendors who are not registered for GST. You have to pay the GST directly to the government for these purchases.

3. Revised Invoices:

Old invoices that you have updated or corrected.

4. Debit Notes:

Documents you send to customers if there are additional charges after the sale, like extra costs or corrections needed after the invoice was issued.

5. Credit Notes:

Documents used for refunds or discounts given to customers after the sale.

6. Receipt vouchers:

Documents you give to customers when you send out goods along with a delivery note, but without an invoice.

7.Payment Vouchers:

Documents you provide to customers when they make payments against your invoices.

8.Refund Vouchers:

Documents that detail any refunds made to a customer, including information like the GST numbers of the parties involved, the goods or services refunded, the refund amount, and the date of the refund.

9. Delivery Challans:

Documents that record when goods are sent from your warehouse to another location. They are used for various reasons, like job work or sending goods for approval, and are categorized into different sections based on the type of supply.

At the end of the document, there is a declaration of truth that needs to be signed by the authorised signatory of your company.

Related Posts