GST refund: What is a provisional order for a refund?

Published on: Thu Jan 30 2025

Krishna Chaurasiya

GST refund: What is a provisional order for a refund?

A provisional refund in GST offers exporters and businesses temporary access to funding until their complete refund is processed. Provisional refunds serve as an urgently needed method to supply quick financial relief for exporters whose delayed GST claim processing impacts their short-term cash flow situation.

What is a Provisional Refund Order?

Through the Provisional Refund Order structure of Goods and Services Tax (GST), businesses can access accelerated refund in GST payments even while their review process is still pending. Businesses can control their cash flow needs by receiving partial payment through this system while their complete claim verification completes. Under Section 54(6) of the CGST Act, 2017, businesses can receive 90% of their refund in GST amount as initial reimbursement. The 10 percent balance only releases after the verification requirements are successfully met.

A business qualifies for an advance refund in GST by submitting Form GST RFD-04 with their application. Selected GST officers can authorize up to 90% of requested refunds without performing full checks of documents. Businesses can preserve their working capital during the assessment period thanks to the provision of 90% early refund amounts. The final refund processing produces either total reimbursement through Form RFD-06 or absolute rejection using Form RFD-08. A discrepancy between the provisional and final refund amounts will require an adjustment. When a refund denial happens businesses need to restore the previously granted provisional refund money.

Provisional refunds are mainly given in cases where the business is involved in zero-rated supplies, such as:

- Exports of goods or services.

- Supplies to Special Economic Zone (SEZ) units and developers.

A GST officer will grant a refund in GST sum following application assessment without input tax credit adjustments. The refund processing procedure according to Form RFD-02 takes seven days or less after application acknowledgment to transfer funds directly to the applicant's account with Form RFD-05 payment advice.

A provisional refund is unavailable to those applicants who have faced tax evasion charges exceeding ₹2.5 crore within the past five years.

Eligibility Criteria for Provisional Refunds

To be eligible for a provisional refund under GST, businesses must meet certain conditions:

- No Major Tax Evasion History: A company cannot claim tax evasion penalties for evaded tax liabilities exceeding ₹250 lakh over the preceding five tax years and the approved refund time period.

- GST Compliance Rating: A business qualifies for a provisional GST refund as long as its internal auditors rate their performance at five or higher on the available scale.

- No Ongoing Legal Issues: Transaction eligibility depends on the fulfillment of two requirements: the absence of pending legal proceedings linked to the refund petition alongside no major history of tax avoidance. Any cases that meet the criteria cannot be temporarily suspended by relevant governmental bodies.

Application Process for Provisional Refunds

1. Filing the Refund Application:

- A loss application through online channels utilizing GST RFD-01 requires all necessary information on the GST portal.

- You must provide all refund in GST claim information and necessary supporting documents when submitting this form.

2. Acknowledgment of Your Application:

- When you submit your application, it will trigger an acknowledgment message confirming receipt. This will happen within 15 days.

- Tracking your application becomes possible with the reference number (known as ARN) you get after filing your submissions.

3. Review of Your Application:

- A GST officer reviews your submitted application together with the documents you provided. The officer will issue a GST RFD-03 notice to request necessary corrections whenever your application contains missing information or mistakes.

- The tax department needs fifteen days to issue such a notification beginning from the date they receive your application document or afterward.

4. Provisional Refund Approval:

- The GST officer will issue a provisional refund for 90 percent of your total request amount when every document passes inspection properly.

- A provisional refund will reach your account within seven days after your application gets confirmed.

5. Final Refund Decision:

- The GST officer will accept or decline your remaining GST refund request through their careful evaluation process.

- You should expect a decision on your final refund amount during the 60-day period after our system notes your application.

- The refund will enter your bank account upon approval. The rejected portion of a refund payment either lands in your credit ledger or offsets your taxable obligations.

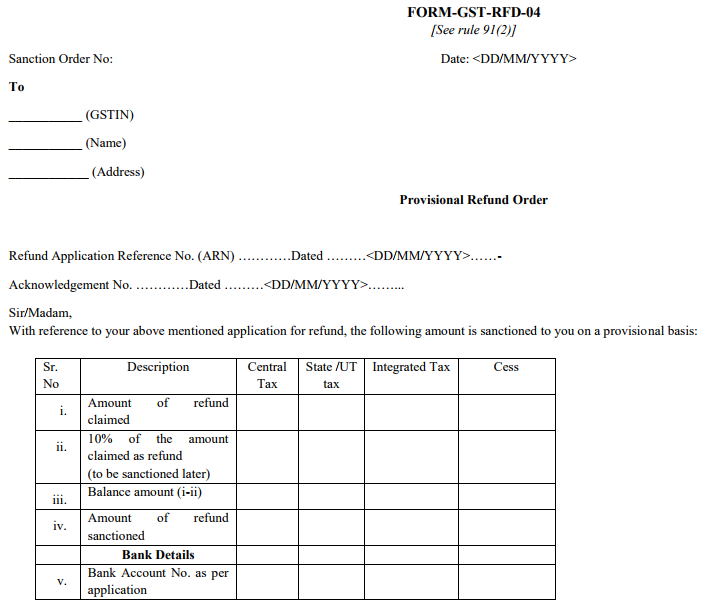

Overview of Form GST RFD-04

The GST officer uses Form GST RFD-04 to authorize a provisional 90% refund of the claimed amount. Through this form, the taxpayer receives an official confirmation about the provisional refund approval from authorities. The issue of this form is essential for the GST refund process to grant prospective financial relief to taxpayers during the time when final verification is in progress.

Contents of the form RFD-04

- ARN / Refund Application Number with date

- Acknowledgement Number (as per RFD-02 ) with date

- The amount of refund in GST claimed by the applicant, the balance amount left to be refunded later (10% of refund claimed), and the amount sanctioned now on a provisional basis will be given under each category of tax: IGST or CGST and SGST/UTGST with cess if any.

- Point to be noted that the balance amount arrived at (iii) as per the form and the Provisional Refund sanctioned at (iv) need not be the same.

- Amount at (iv) can be less than or equal to the amount arrived at in (iii)

At last, details of the bank account to which the refund amount is credited shall be mentioned in the form.

The GST officer reviews both the submitted application and supporting documentation that taxpayers present for a GST refund. After finding the claims genuine, the officer issues Form RFD-05 payment advice and their final refund sanction order.

When an officer suspects unjust enrichment because the claimant shifted tax costs to the buyer who took Input Tax Credit (ITC) for matching supplies, they may redirect the refund to the Consumer Welfare Fund. The fund requires applications from aggrieved persons who must accompany their applications with supporting documents and statements that validate their claim.

However, the following scenarios are exceptions to this rule:

- Claimants can receive GST tax refunds for exports of goods or services with zero rates through paid IGST or ITC payments processed under a Letter of Undertaking (LUT).

- A company can obtain reimbursement for untapped tax credits established through inverted duty structures.

- Tax refunds apply when suppliers cancel their service entirely or partially before invoicing.

- The system allows tax cash refunds when claimants demonstrate that tax costs remain unpaid by others or third parties.

- Additional refund in GST applications come under the government's specifically published guidelines.

Timeline for Provisional Refund Processing

- Acknowledgment: A refund acknowledgment will be sent to you within 15 days of submitting your application.

- Review and Request for Corrections (if needed): Your application gets reviewed within 15 days from submission.

- Provisional Refund Issued (Form GST RFD-04): The system acknowledges the application within 7 days after processing.

- Final refund in GST: The certification process takes 60 business days from the time your application receives initial acknowledgment.

Limitations of Provisional Refunds

- Registered persons can receive provisional refunds only if they have never had legal action filed against them for substantial tax evasion that surpassed ₹2.5 crore during the past five years.

- The amount of the provisional refund cannot exceed 90% of total claimed amount without consideration of previously accepted input tax credit.

- A proper officer needs to issue the refund order not later than seven days from the date they acknowledged the refund application.

- The refund procedure faces potential withholding for individuals who either fail to file tax returns or fall behind on their tax payments.

Scenarios Where Provisional Refunds Apply

- Zero-rated export transactions qualify for provisional refunds through which exporters can obtain input tax credit refunds for export goods leaving Indian territory.

- For situations when input tax rates exceed output tax rates (inverted duty structures), businesses can obtain provisional refunds of their unused input tax credits.

- Deemed exports operating within national borders through internal export mechanisms qualify for provisional refunds.

Challenges in Provisional Refund Applications

- An incorrect combination of tax invoices and shipping bills, alongside a demonstration of tax payments, often results in delayed or rejected refund claims.

- A two-year deadline for submitting applications presents significant challenges because determining the eligible date remains complex according to different types of claims.

GST refund applications get rejected when businesses fail to satisfy their obligations to pass along tax costs to their customers.

Best Practices for Provisional Refund Compliance

- A proper record system of tax invoices together with shipping bills and tax payment records enables effortless refund claim processing.

- Both provisional refund processing and application filing require strict attention to established time constraints that include maximum application periods of two years as well as seven-day periods for provisional refunds.

- Knowledge of the eligibility standards for provisional refunds will help you prevent refunds from being turned down.

- Dependency on GST provisions and awareness of regulatory changes require regular review to achieve regulatory compliance and uncover additional refund in GST options.

Through a GST provisional refund businesses including exporters receive partial reimbursement funds during the validation process for their entire claim. The provision provides short-term relief to business cash flow when processing take longer than expected. All qualifying enterprises need to follow set requirements with binding time limits. Businesses receive financial relief through this process yet it maintains operations during the procedure.

FAQs

1. What is a provisional refund in GST?

Through a provisional refund system, businesses can obtain a maximum of 90% of their applied GST refunds while waiting for the complete verification process to finish. The provision maintains sufficient cash flow for businesses throughout their wait for final refunds as part of their processing time.

2. How can I apply for a provisional refund under GST?

A provisional GST refund application must be submitted using Form GST RFD-04 on the GST portal system. The application needs documented evidence to proceed through successful processing stages.

3. How long does it take to receive a provisional refund?

Your institution will approve your request, and then you can obtain your refund within seven days after receipt of application acceptance.

4. What happens if my provisional refund application is rejected?

You must return previously granted refund amounts after your provisional refund application gets rejected and deal with additional investigation for any identified discrepancies.

At MyGSTRefund, we understand the complexities of the GST refund process, so we have developed several intuitive tools to simplify your refund journey. Our Know Your Refund tool provides valuable insights into your eligibility and helps you track your refund status efficiently. Additionally, our GST Refund Calculator helps you accurately calculate your refund amount, minimizing the chances of errors and increasing the likelihood of a successful refund sanction. These tools are designed to make the refund filing process easier, ensuring you get your rightful refund without unnecessary delays.

Related Posts

")

")